This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified real estate or financial professional before making any investment decisions.

Every year, the Urban Land Institute and PwC release what has become one of the most closely watched documents in commercial real estate: the Emerging Trends in Real Estate report. Drawing on surveys and interviews with hundreds of institutional investors, developers, lenders, and market analysts, the report synthesizes where sophisticated capital is flowing, which markets are gaining momentum, and which are losing it. For anyone trying to cut through the noise of macro headlines and understand where the real estate industry’s most informed participants are actually placing their bets, this report is essential reading.

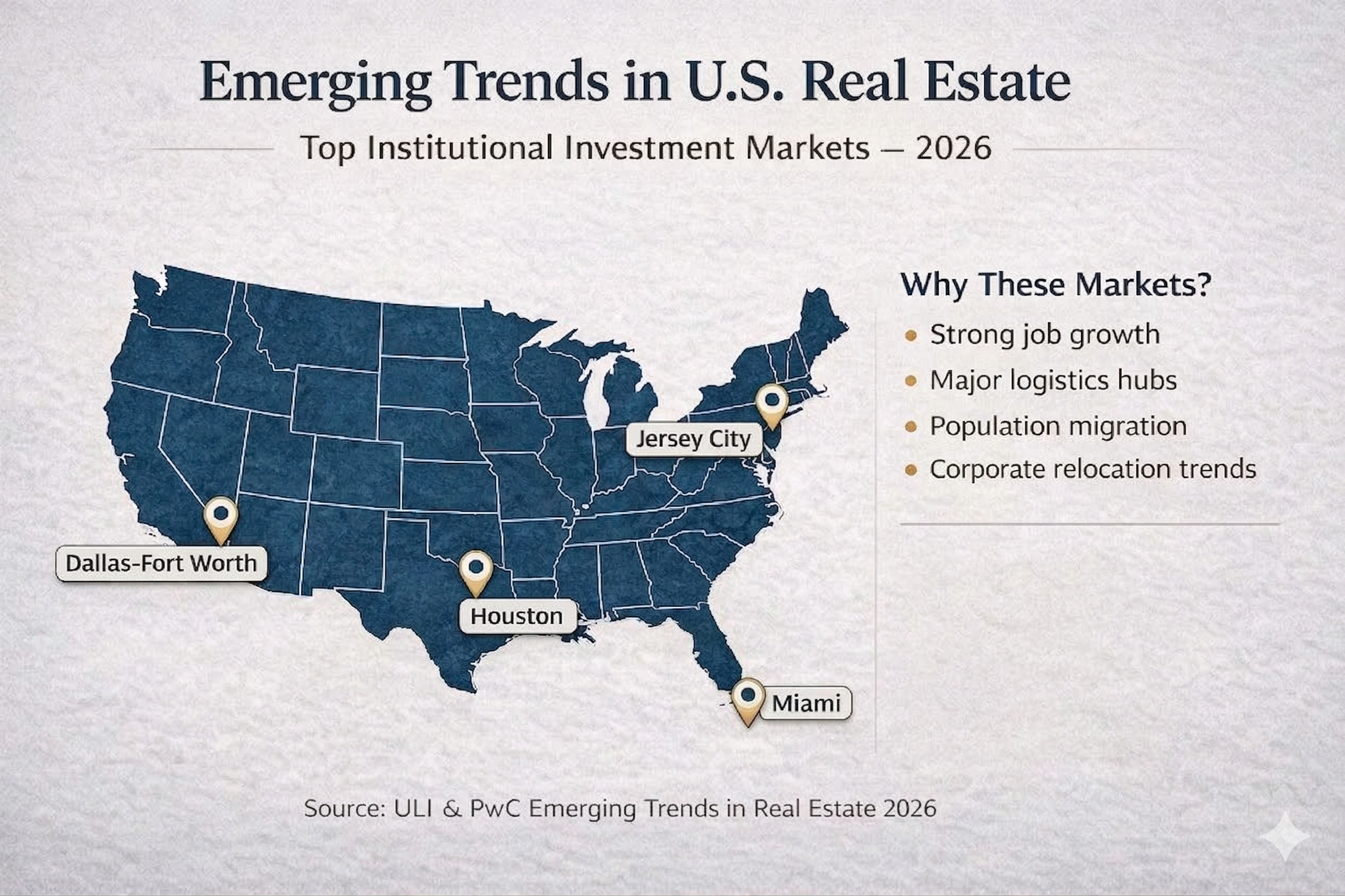

The 2026 edition ranks more than 80 U.S. metropolitan areas by their overall real estate prospects. What emerges from this year’s rankings is a picture of a market that continues to reward infrastructure advantages, business-friendly policy environments, and relative affordability — while punishing markets that have allowed costs, regulation, or structural oversupply to erode their competitive position. The top five metros on this year’s list reflect those dynamics clearly. Here is what the data says about each of them.

Dallas–Fort Worth: Holding the Top Spot for the Second Consecutive Year

Dallas–Fort Worth retaining the number one ranking for the second year running is not a surprise to anyone who has been tracking its fundamentals. What is notable is the breadth of the case for DFW — it is not a story about one asset class or one industry. It is a story about a metro that has assembled nearly every ingredient that institutional real estate capital looks for in a long-term market.

Job creation in DFW has been among the strongest of any major U.S. metro, driven by a diversified economy that spans finance, technology, logistics, and healthcare. The region has attracted roughly 100 corporate headquarters relocations since 2018 — a figure that reflects not just tax policy but genuine quality-of-life and talent pool advantages. Texas has no state income tax, and DFW’s regulatory environment is consistently described by developers as among the most streamlined of any large metro in the country.

The industrial and retail sectors both carry net buy recommendations in this year’s report, reflecting strong demand fundamentals and favorable supply-demand dynamics. The office market tells a more complex story — but an interesting one. More than 20 office-to-residential conversion projects are underway, collectively repositioning approximately six million square feet of office space into housing. That conversion activity is not just a response to office vacancy; it is evidence of a market with the population growth and housing demand to absorb repurposed product.

DFW is also the second-largest financial center in the United States, a fact that is often underappreciated by observers focused on coastal markets. The combination of financial sector depth, logistics infrastructure anchored by one of the world’s busiest airports, and continued corporate relocation activity positions DFW as one of the most durable real estate investment destinations in the country heading into the second half of the decade.

Jersey City: The Biggest Mover on This Year’s List

Jersey City’s jump of 17 places on this year’s rankings is the most dramatic single-year move in the top tier of the report, and the data behind it is compelling. Between 2020 and 2024, Jersey City’s population grew 7.5% — a rate that places it among the fastest-growing urban cores in the Northeast. That population growth is translating directly into multifamily demand that has outpaced a significant supply increase: despite a 20% rise in apartment inventory over five years, multifamily vacancy sat at just 2.8% in Q2 2025. Same-store rents rose 2.4% over the prior 12 months — double the national average.

The office market dynamics along the Hudson River waterfront are equally instructive. Average asking rents in Jersey City, Hoboken, and Weehawken reached $44.51 per square foot — 32% above the broader Northern New Jersey market, yet still 42% below Manhattan. For tenants who need proximity to New York’s financial district but cannot absorb Manhattan rents, that spread represents a powerful value proposition. Waterfront vacancy declined to 24.6% from 25.8% at year-end 2024, and the finance, insurance, and real estate sector accounts for roughly 63% of leasing activity — a concentration that reflects Jersey City’s genuine functional integration into New York’s financial ecosystem.

The broader investment thesis here is straightforward: Jersey City is capturing overflow demand from one of the most expensive and constrained real estate markets in the world. With quick ferry access to Manhattan, a growing inventory of lab space, and high-rise development that would be economically impossible to replicate in Manhattan at comparable price points, Jersey City offers a combination of urban amenity and relative affordability that continues to attract both residents and employers.

Miami: The Global Gateway That Keeps Strengthening Its Position

Miami slips one spot to third place, but a one-position decline from second to third in a report of this caliber is not a signal of weakness — it is a reflection of how strong the competition at the top of the list has become. Miami’s fundamentals remain exceptional, and in several respects they are getting stronger.

The case for Miami is anchored in infrastructure that most metros cannot replicate. Miami International Airport handles approximately 85% of U.S. air imports and 80% of exports to Latin America and the Caribbean — a logistics position that makes the metro a genuine gateway between North American and Latin American economies. PortMiami moved more than 1.12 million TEUs in the most recent fiscal year and ranks among the nation’s busiest container ports. That infrastructure does not just support trade — it supports the entire ecosystem of logistics, warehousing, financial services, and professional services that depends on it.

The office market data reflects Miami’s appeal to international and domestic tenants alike. According to Cushman & Wakefield, average asking office rents reached $64.48 per square foot at the end of 2025 — up 10.2% year over year — with Class A rents climbing to $70.39 per square foot. Vacancy improved to 15.2%, down 70 basis points from the prior year. Looking across a five-year horizon, Miami office rents have risen more than 52%, a trajectory that reflects sustained demand from corporate relocations spanning technology, finance, and professional services.

Florida’s absence of a state income tax remains a meaningful draw for both businesses and high-income individuals. The wave of corporate relocations that began during the pandemic years has not fully reversed — it has evolved into a more permanent reconfiguration of where certain industries choose to locate. For real estate investors, Miami offers a rare combination of institutional-grade asset quality, strong rent growth, and a demand base that is diversified across domestic and international sources.

Brooklyn: From Secondary Borough to Primary Market

Brooklyn’s ten-place jump on this year’s rankings tells a story that has been building for years but is now arriving at full institutional recognition. The borough is no longer being evaluated as an extension of Manhattan — it is being evaluated as a primary real estate market in its own right, with its own demand drivers, its own industry clusters, and fundamentals that in some respects outperform the broader New York metro.

The residential numbers are striking. Brooklyn’s median free-market rent reached $3,804 in late 2025, an 8.7% year-over-year increase. Vacancy sits at approximately 2% — one of the lowest rates of any major market nationally. Cumulative rent growth since 2019 stands at 44%, a figure that reflects genuine structural undersupply relative to sustained demand. These are not the numbers of a secondary overflow market. They are the numbers of a market with its own gravitational pull.

The office market has followed a similar trajectory. Select Brooklyn submarkets have recorded falling vacancy and rising asking rents, driven by demand from creative industries, life sciences tenants, and businesses that want proximity to Manhattan talent pools without Manhattan pricing. The limited new supply pipeline in Brooklyn — constrained by land costs, zoning complexity, and development economics — means that the supply-demand imbalance underpinning current rent levels is unlikely to resolve quickly.

For institutional investors, Brooklyn represents something increasingly rare: a dense, amenity-rich urban market with genuine affordability advantages relative to its primary neighbor, strong demographic momentum, and a diversifying economic base that reduces concentration risk.

Houston: Logistics Scale and Affordability in a Heavyweight Market

Houston slips two places to fifth but remains one of the most institutionally significant real estate markets in the country. The case for Houston has always been anchored in scale — and the scale here is genuinely impressive. The Port of Houston handles 74% of U.S. Gulf Coast container traffic and 97% of Texas container volume. The metro’s manufacturing base includes more than 7,000 manufacturers producing over $75 billion worth of goods annually. More than 500 aerospace and aviation firms operate in the region.

That industrial and logistics infrastructure creates durable real estate demand that operates largely independently of the office market cycle. Houston’s office vacancy remains elevated — a legacy of energy sector contraction and remote work adoption — but the industrial and logistics sectors tell a different story, one defined by sustained occupancy and rent growth driven by the port and the manufacturing base it serves.

Residential affordability is a genuine structural advantage. Houston’s median home sale price runs approximately 20% below the national average — a spread that, combined with Texas’s absence of a state income tax, continues to attract both population and corporate investment. The energy and medical center economies provide employment diversity that distinguishes Houston from single-industry markets, and the metro’s continued population growth supports homebuilding and multifamily demand despite the office market headwinds.

What These Five Markets Have in Common

Looking across the top five markets, several patterns emerge that are worth internalizing as investment principles rather than market-specific observations.

Infrastructure matters more than ever. Houston and Miami rank among the nation’s busiest port complexes. DFW operates one of the world’s largest airport systems. Jersey City’s ferry and transit connections to Manhattan are its defining competitive advantage. In each case, physical infrastructure creates demand that is structural rather than cyclical — it does not evaporate when sentiment shifts.

Tax and regulatory policy is a genuine differentiator. Texas and Florida have both built significant competitive advantages through the absence of state income taxes and the cultivation of business-friendly regulatory environments. The corporate relocation numbers in DFW and Miami are not coincidental — they are the direct result of sustained policy choices that have compounded over years.

Relative affordability remains one of the most powerful demand drivers in real estate. Jersey City and Brooklyn are both benefiting from their position as more affordable alternatives to the most expensive market in the country. DFW and Houston offer meaningful cost advantages over coastal peers. In an environment where affordability is under pressure across the board, markets that offer comparable quality at lower cost have a structural tailwind.

Diversified demand bases reduce risk. The strongest markets on this list — DFW, Miami, Houston — are not dependent on a single industry or employer base. That diversification does not eliminate cyclicality, but it does reduce the severity of downturns and the duration of recoveries.

The 2026 ULI and PwC rankings reinforce a conclusion that has been building for several years: market selection is the most important variable in commercial real estate investment, and the markets that combine infrastructure advantages, policy competitiveness, relative affordability, and diversified demand are increasingly separating themselves from the rest of the field.